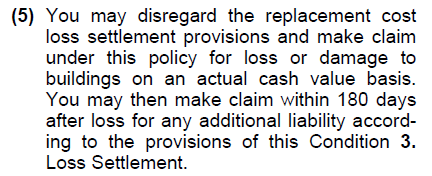

In a prior post, we told you all about the Statute of Limitations (SoL), and how homeowners and businessowners who suffer a catastrophic property loss must – with limited exception – file suit “for the recovery of any claim by virtue of this policy” within the time limits required by the state-mandated SOL. If the SOL is two years, as it is in Massachusetts, then insurance claimants must file suit within two years of the date of loss, regardless of when the policyholder first became aware of the loss.

However, there’s a wrinkle that often causes massive confusion. Most policies also provide replacement cost coverage for new materials of like kind and quality to replace older, depreciated property that has been damaged. But the policies providing this additional amount do not make that coverage available until the policyholder incurs the cost of replacement and the work is actually done.

Most replacement cost policies have this provision in the main document:

As if this wasn’t confusing enough, the loss settlement provisions in most policies dictate:

We will not pay on a replacement cost basis for any loss or damage:

(1) Until the lost or damage property is actually repaired or replaced; and

(2) Unless the repair or replacement is made as soon as reasonably possible after the loss or

damage.

Recently, we have encountered insurance adjusters (usually from national companies rather than local ones) who insist on the 180-day limit contained within the policy as the time limit after the loss controlling when replacement must be achieved. This is not a correct position. The typical Massachusetts Changes Endorsement, required under Mass. Gen. Laws ch. 175. § 47. clause 17, amends the Replacement Cost provision states:

- We will not pay on a replacement cost basis for any loss or damage:

(1) Until the lost or damaged property is actually repaired or replaced:

(a) On the described premises; or

(b) At some other location in the Commonwealth of Massachusetts; and

(2) Unless the repairs or replacement are made within a reasonable time, but no more than 2 years after the loss or damage.

This means that policyholders have two years from the date of loss to make repairs in order to qualify for the “holdback,” which is the difference between the amount paid for “Actual Cash Value”, i.e. the amount of damage after depreciation is considered, and the amount due for “replacement cost”, i.e. new for old. And this contracted limit of time usually applies whether or not the parties have actually agreed on the amount of loss or had it determined by the reference/arbitration/appraisal procedure.

As a practical matter, this requires policyholders to assume the risk that the cost of performing those repairs would be fully reimbursable by the insurer, and that any dispute about the cost of the repairs would be resolved in their own favor unless the policyholder is fortunate enough to have cash on hand or an understanding bank.

While obviously one-sided in favor of insurers, this situation has been found in a recent case to be legal under the policy terms. In R.R. Ave. Props. • LLC v. Acadia Ins. Co., 37 F.4th 682 (1st Cir. 2022), the United States Court of Appeals for the First Circuit in Boston recently dealt with a situation involving a major fire in a commercial building. The insurer and the policyholder quickly agreed on the amount of replacement cost and actual cash value. The insurer promptly paid the actual cash value amount, but declined to pay the “holdback” unless and until the work was completed. For reasons that were not clear, although the policyholder entered into a construction contract early on, no work was started until shortly before the two-year contractual period was due to run. The policyholder requested an extension of several months, but the insurer refused – as most insurers commonly do.

The Court held that the policy required “actual” repair/replacement, not substantial completion, and that the mere execution of contracts and payments alone did not satisfy the policyholder’s obligations. Finally, the court rejected the insured’s arguments under the implied covenant of good faith and fair dealing and held the insurer was under no obligation to grant the requested extension. This is a harsh decision, though perhaps understandable given the unexplained inactivity of the policyholder.

In another recent case in Massachusetts, a woman had extensive steam damage to her home resulting from a burst boiler fitting. She and her insurer disputed the amount of damage and the matter was sent to be decided by referees. The referees made a very favorable ruling for her, but it came more than two years after the date of loss. Although case law holds that an insured isn’t required to rebuild until they know how much they are going to be paid, and although the woman had requested an extension of the two-year contractual period months before it expired, the Judge refused to order the insurer to pay the holdback amount due her because of the failure to complete repairs within two years.

There are other cases around the country (but not in Massachusetts) where unforeseen circumstances, such as interference by building officials, Covid, delay by the insurer, etc., have justified an extension of the contractual period to rebuild for equitable reasons in order to avoid an unjustified forfeiture. But those circumstances are rare.

The better course for policyholders and their representatives to follow is to try to reach agreement on the amount due as soon as possible and begin work quickly. If circumstances arise which prevent moving ahead, document these and report them to the insurer. Otherwise, it is quite easy to be SOL on this two-year contractual limitation period.