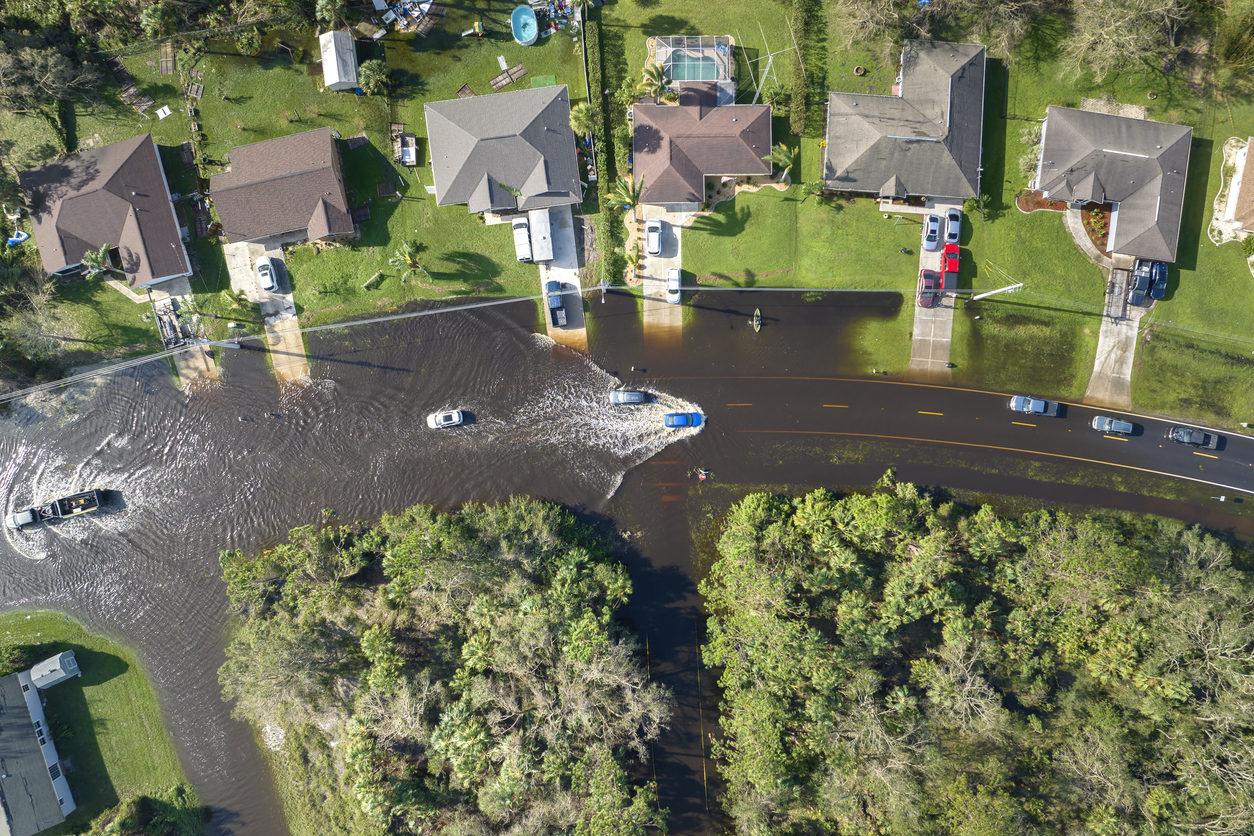

With all of the recent storms tearing through the coast of New England, SMW’s loyal client base has been “flooding” our offices with calls for help to assist with the handling of these claims. Below is a quick description of the flood policies that we encounter while working on these claims. But…. What if a heavy windstorm happens concurrently with the flood, and how does this tie into the claim? Flood policies don’t cover windstorm damage, and property polices usually don’t cover flooding. What came first, the chicken or the egg? What happened first or second? What happens if there is anti-concurrent causation language in the policy? These can be an absolute nightmare to unravel.

First off, let’s understand exactly what floods entail, as far as your National Flood Insurance Program (NFIP) policy is concerned. In most NFIP policies, “Flood” means:

- A general and temporary condition of partial or complete inundation of normally dry land areas due to any of the following:

(1) Overflow of inland or tidal waters from a natural or man-made body of water, including:

(a) Waves, such as tidal wave and tsunami;

(b) Storm surge; and

(c) Spray from any such overflow; all whether driven by wind or not

(2) Unusual or rapid accumulation or runoff of surface waters from any source, including release of water from a:

(a) Dam;

(b) Levee;

(c) Seawall; or

(d) Other similar boundary or containment system; or

(3) “Mudslide or mudflow” caused by flooding as defined in 5.a.(1) and 5.a.(2) above.

b. Collapse or sinking of land along the shore of a body of water as a result of erosion or undermining caused by waves or currents of water which exceed cyclical levels and cause flooding as defined in 5.a.(1) above.

All flooding in a continuous or protracted event will constitute a single occurrence of “flood”.

With that definition in hand, let’s understand another important point about your NFIP coverage: It’s intended to get homeowners some relief – not make them whole.

Now let’s get to the next key question: are you covered? If you only have a flood policy through NFIP, then the answer may be ‘No.’ In residential policies, the coverage limit for a single-family residence is $250K for the structure and $100K for personal property. The maximum coverage limit for businesses is $500K for the building and $500K for your business personal property.

This is important to understand because, in our experience, people who buy a flood policy through NFIP think they have comprehensive flood insurance. This is a myth! In fact, these policies are not only limited by dollar values but also are limited in what they cover. NFIP policies are limited when it comes to damage that is below-grade – that is, related to flooding. These policies mainly cover unfinished drywall, insulation, mechanicals, plumbing, electrical but not paint, wallpaper and flooring.

So, if you have a policy through NFIP, read through it very carefully to understand what is covered and what is not. If you want full flood insurance protection, you will have to purchase a complementary policy through a private insurance provider – it may be costly depending on the location of your property. It will be worth it, of course, in the event of major flood damage.

But if you only have a flood policy through NFIP, give it a good read and understand what it actually covers. Remember: it’s only supposed to help you get you back on your feet – not make you entirely whole after a flood loss.

Now let’s talk about the property policy for a moment and how that could come into play. Oftentimes when there is a major storm, there are both windstorm and flooding damages. As we stated at the beginning of this blog, flood policies don’t cover windstorm damage and property polices usually don’t cover flooding. So how do we unravel all of this? Unless you have a ring camera set up to show the entire storm and what event happened in what sequence, it’s a major challenge to decipher multiple issues potentially happening at the same time.

To further complicate this jumbled matter, what happens when there is anti-concurrent causation language in the policy? The premise of anti-concurrent causation is that if there are multiple causes of loss involved in a claim and one of those causes is excluded from coverage (although the others may be covered), the entire loss is not covered. This is why it’s crucial to RTFP!

We recently ran into this exact scenario. The insurance company’s adjuster stated that due to the anti-concurrent causation language, none of the windstorm damage was covered. However, when SMW did some digging, we located the ring camera footage. Lo and behold, the video clearly showed the windstorm damage occurring hours before the flooding, and we were able to get all of the windstorm damage covered on the property policy.