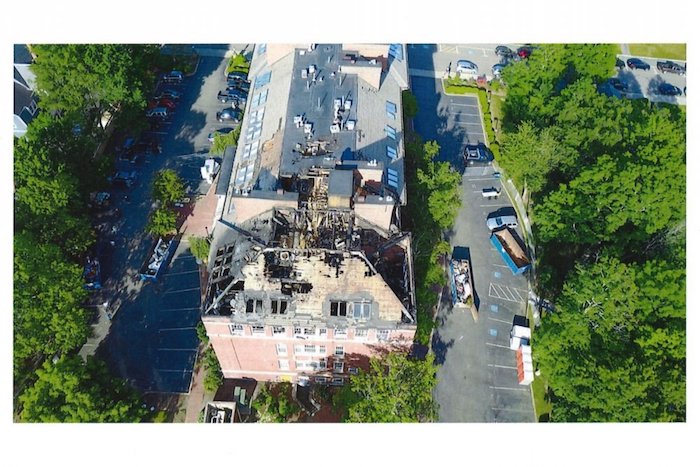

We recently handled a property loss at a large condominium complex. The building suffered a huge fire, and all unit owners had to move out. The structure was uninhabitable and there was no building left to maintain or common area lights to keep on.

But: the association still had to pay property taxes. It also had to continue paying its management company. Moreover, the town still required the condo to maintain its lawn to keep it from becoming a public nuisance.

Obviously, these traumatized unit owners didn’t want to pay fees if they weren’t getting the benefit of the property. So, what happened? The unit owners stopped paying their condo fees.

In this case, the association had an insurance policy that reimbursed it for the condo fees that the unit owners did not pay. But it’s not as simple as adding up the monthly fees of each unit owner and multiplying by the number of months they were out. There remain several expenses that you don’t actually have to continue paying. Take, for example, the condo’s common area lights, its alarm service, or general repairs.

So, the insurance company hired a forensic accountant to review the books and records of this association and determine the overall net loss (calculated by lost revenue MINUS the discontinued expenses).

In this particular case, however, the participating accountants took an unorthodox view on the saved expenses. How so? The year before the loss, the association hired a tree pruning company to trim the trees. That’s an expense the association only has to incur once every few years, if that. But the insurance company’s accountant projected that as an annual expense for the association throughout the loss period.

Here are a few more examples to consider:

Insurance expense – Because the property is uninhabitable, the condo association now must buy a builder’s risk policy (which costs more than standard coverage). So, their insurance premiums will increase as a result of this loss. The accountant didn’t include this increase as part of the loss calculation. Remember, if the carrier takes the credit for a discontinued expense, they must also include the increase as part of the loss calculation.

Vent cleaning – This is another example of a service that insurance accountants often take as a savings, when some buildings – like this one – don’t clean the vents every year.

Landscaping – The insured might actually spend more to beautify and make the post-fire area look nice. But the insurance company could claim that those expenses are not related to the loss and could move to discontinue the expense in full.

These are simple items, but sometimes the insurance company won’t initially get the right answers – and it’s up to you to correct them. The insurance company is content to let the accountant take the lead – and they are not adjusters – so there can be a lack of oversight to this. The insurance company will rely solely on the projections by the hired accountant, but these professionals might not understand the nuances described above.

The point is – if unit owners can’t use the property in the fashion that they purchased, why should they keep paying for the use of it? Imagine if the loss occurred in a 10-unit building, for example, but only 5 units were affected. Why should the affected units keep paying, while the others (the unaffected units) continue enjoying the benefits?

It goes back to what the unit owners would have paid if there had been no loss. The idea is to put the association owners back in the position they would be in if no loss occurred at all.

If the insurance company doesn’t recognize this somewhat complicated calculation, it might end up in Reference – at which point a 3-person panel would likely recognize that the accountant’s views did not make sense. Understanding these points can save everyone money from the outset!